Diamond Industry Navigates Volatility as Geopolitical Tensions and Trade Barriers Reshape Global Markets

The global diamond industry faced a tumultuous period throughout March 2026 as a confluence of geopolitical instability, shifting trade policies, and corporate restructuring created a deeply fragmented market environment. While the high-end luxury sector showed resilience through sustained demand for large, high-quality stones, the broader market struggled under the weight of escalating conflict in the Middle East and ongoing trade friction between the United States and India. According to the latest data from the RapNet Diamond Index (RAPI™), price corrections were observed across several key categories, reflecting a cautious sentiment among global dealers and a logistical paralysis in major trading hubs.

The primary driver of market uncertainty was the outbreak of a significant conflict in the Middle East, which began on February 28, 2026. By March, the situation had escalated into a broader regional crisis, marked by Iranian missile strikes that effectively brought commercial activity to a standstill in two of the world’s most critical diamond centers: Dubai and Israel. As trading floors in the Dubai Multi Commodities Centre (DMCC) and the Israel Diamond Exchange in Ramat Gan faced unprecedented operational halts, the industry’s midstream—the vital link between rough mining and retail distribution—experienced a severe bottleneck.

Geopolitical Shockwaves and the Frozen Middle East Hubs

The timing of the conflict, starting in late February, disrupted the traditional spring trading momentum. For decades, Dubai and Israel have served as the "engine rooms" of the diamond trade, facilitating the movement of billions of dollars in rough and polished goods. The Iranian missile strikes in March forced many firms to shutter operations temporarily, leading to a "freeze" in local trading. This paralysis had an immediate ripple effect on the global supply chain, as goods intended for European and American markets were stalled in transit or held in secure vaults.

In response to the security risks, major rough diamond tender houses were forced to relocate their planned sales events. Traditionally held in Dubai due to its favorable tax environment and geographical proximity to both African mines and Indian cutting centers, these auctions were moved to alternative locations to ensure the safety of participants and the security of the inventory. This logistical shift added significant costs and delays to the procurement process, particularly for Indian manufacturers who rely on a steady flow of rough stones to keep their factories in Surat and Mumbai operational.

US-India Trade Relations and the Tariff Burden

Parallel to the physical disruptions in the Middle East, the industry continued to grapple with trade barriers between the world’s largest consumer market—the United States—and its primary manufacturing hub, India. US tariffs on Indian-finished diamond goods have remained a persistent concern for dealers. Although these tariffs were lowered to 10% in February 2026, the industry had hoped for a more significant reduction or a total waiver to stimulate trade.

The 10% tariff continues to squeeze the margins of Indian exporters, who are already facing rising energy costs and fluctuating labor availability. For New York-based wholesalers, the cost of importing commercial-quality stones from India has become a point of contention in price negotiations with retailers. Many US retailers are hesitant to absorb the additional costs, leading to a standoff that contributed to the downward pressure on the RapNet Diamond Index for smaller, mass-market stones.

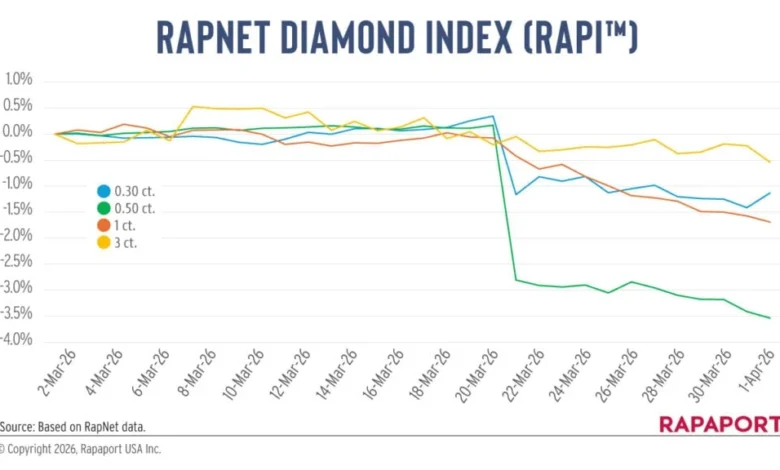

Analyzing the RapNet Diamond Index (RAPI) Performance

The March performance of the RapNet Diamond Index (RAPI™) highlighted a clear divergence in value based on stone size and quality. The index, which tracks the average asking price for the 10% lowest-priced round diamonds in the top 25 quality categories (D-H, IF-VS2), showed declines across all major weight classes:

- 1-carat diamonds: The RAPI for this benchmark category fell by 1.7% in March.

- 0.30-carat diamonds: This category saw a decline of 1.1%.

- 0.50-carat diamonds: This segment experienced the sharpest drop, falling 3.5%.

- 3-carat diamonds: Large stones were the most stable, with the index dropping only 0.5%.

The significant drop in 0.50-carat stones reflects a surplus of inventory in the "commercial" range, where consumer demand has softened due to economic headwinds and the continued competition from laboratory-grown diamonds. Conversely, the relative stability of the 3-carat index underscores the "flight to quality" and the enduring appeal of high-value natural diamonds as a store of wealth during times of geopolitical crisis.

Price List Adjustments and Market Reaction

On March 20, the Rapaport Price List—the industry’s primary benchmark for diamond valuation—was adjusted downward for round diamonds up to 1.99 carats and pear-shaped diamonds up to 0.99 carats. Such adjustments often trigger volatility in the market, but the reaction this time was notably measured. Rapaport CEO Dan Mano issued a public message following the changes, providing context on the necessity of the adjustments in light of current market realities.

Industry analysts noted that Mano’s transparency helped prevent panic selling. By acknowledging the pressures of the Middle East conflict and the tariff situation, the message allowed dealers to recalibrate their expectations. This "measured" reaction suggests a level of maturity in the current market, where participants are increasingly relying on data-driven insights rather than emotional responses to global events.

High-End Resilience: Polished and Rough Demand

Despite the overall index declines, the high-end segment of the market remained a bright spot. Polished diamonds of 2 carats and larger, particularly those in "long fancy shapes" such as ovals, emerald cuts, and marquises, were in high demand but remained in short supply. New York wholesalers reported steady orders from luxury retailers, who noted that high-net-worth consumers remain largely insulated from the inflationary pressures affecting the middle class.

The scarcity of these large, high-quality stones is rooted in the rough diamond market. At De Beers’ March sight, reports surfaced of price increases for rough stones of 5 carats and larger. Despite the logistical hurdles in Dubai, the appetite for large rough remains aggressive because the yield of high-value polished stones is guaranteed to find a buyer in the current luxury climate.

Strategic Consolidation: De Beers and Signet Jewelers

The month of March also saw significant structural shifts within the industry’s largest players. De Beers, the world’s leading diamond company by value, announced a major reduction in its sightholder list. For the new contract period beginning July 1, the company removed between 20 and 25 sightholders from its previous list of 69 clients.

This "sightholder cull" is a strategic move intended to increase efficiency and ensure that rough supply is directed toward the most financially robust and technologically advanced manufacturers. It also reflects a broader reality of the 2026 market: a long-term reduction in overall rough supply as older mines reach the end of their lifespans and fewer new discoveries are brought online.

In the retail sector, Signet Jewelers—the world’s largest retailer of diamond jewelry—reported its fiscal results for the year ending January 31. The company posted sales of $6.81 billion, a modest 1.6% increase over the previous year. While the growth was slight, Signet’s strategic pivots were more telling. The company announced the closure of its James Allen e-commerce site, absorbing the brand into Blue Nile.

This consolidation is significant because Blue Nile will now pivot its focus primarily toward natural diamonds. This move is seen by many as a strategic bet on the long-term value of natural stones over lab-grown alternatives, which have seen rapid price depreciation over the last 24 months. By streamlining its digital footprint, Signet aims to dominate the high-end natural diamond e-commerce space.

Timeline of Key Events in March 2026

- February 28: Conflict begins in the Middle East, immediately impacting logistics in Israel.

- Early March: Iranian missile strikes lead to the suspension of trading in Dubai and Ramat Gan.

- Mid-March: De Beers holds its third sight of the year, increasing prices on large rough (5ct+) while reducing the total number of sightholders for the upcoming contract period.

- March 20: Rapaport Price List updated, reflecting lower valuations for stones under 2 carats.

- March 25: Signet Jewelers announces the merger of James Allen into Blue Nile and a renewed focus on natural diamonds.

- March 31: RAPI data confirms a 1.7% monthly decline for 1-carat benchmark stones.

Broader Impact and Future Implications

The events of March 2026 suggest that the diamond industry is entering a period of "forced evolution." The combination of geopolitical risk and trade protectionism is de-globalizing aspects of the trade that were once seamless. Dealers are now forced to diversify their logistical routes, moving away from a heavy reliance on a few central hubs like Dubai.

Furthermore, the industry is seeing a widening "value gap" between generic, mass-produced diamonds and investment-grade, large-scale stones. As De Beers tightens its client list and Signet refocuses on natural diamonds, the message to the market is clear: the future of profitability lies in transparency, efficiency, and the high-end luxury experience.

As the industry looks toward the second quarter of 2026, all eyes will be on the potential for a ceasefire in the Middle East and the possible renegotiation of US-India trade terms. Until then, the market remains a tale of two halves—struggling at the bottom but remarkably resilient at the top.

{kind=link}